New data from our AvidPay Network revealed spending by middle market companies on financial services has slowed during the past nine months after steadily rising through the height of the pandemic.

This trend is one of several captured by our Middle Market Spending Trends Report, which analyzes millions of payments made by middle market businesses each quarter.

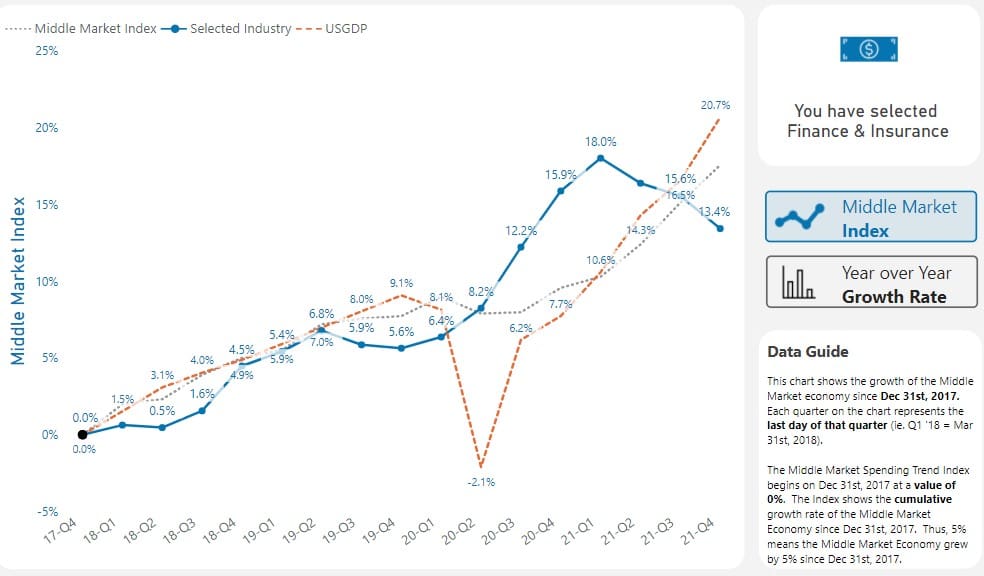

To better understand the trends around financial services spending, let’s start with some key data points.

In the first quarter of 2020, spending on financial services was 6.4% above our December 2017 benchmark, which was when we started tracking middle market spending.

Since early 2020, spending increased each quarter and peaked at 18% above our benchmark following Q1 2021. Then spending fell each of the next three quarters to 13.4% above our benchmark.

It isn’t easy to pin down why spending is declining so quickly after a period of such growth, but our research leads us to believe there are at least three potential culprits:

- The growing fintech market presents a competitive alternative to traditional financial services

- Businesses have fewer funds to allocate toward financial services this far removed from the dispersal of Paycheck Protection Program (PPP) funds

- Rising inflation rates have redirected spending to other business needs

Now let’s explore each of these reasons further:

Fintech solutions vs. Traditional financial services

The fintech market provides various financial services and technologies such as accounts payable (AP) automation that empowers companies to make faster and more secure payments.

During the past year, use of these financial services has become more popular. Many businesses have shifted to electronic payments to continue operating efficiently in the current hybrid working situation.

Given these trends, it’s likely spending by middle market companies on fintech financial services has cut spending on bank financial services, a much larger market than fintech. And this may be a reason why overall spending on financial services has dropped.

Competitive dynamics between fintechs and banks

For deeper perspective, a McKinsey report lays out competitive dynamics between fintechs and traditional banks. On the positive side for banks, the report notes, they have strong and large balance sheets and solid customer relationships cultivated over decades.

“A pessimist, however, would claim that it’s a matter of time until fintechs and big techs replace banks as customer-owners and financial-services providers, relegating banks we know today to the role of balance-sheet operators. A realistic view would be somewhere in the middle.”

Even so, fintechs continue to gain momentum in the financial services industry.

Big-tech companies impacting the financial services industry

“The influence of tech-savvy consumers, looming threat of big-tech companies and shifting attitudes of regulators towards new tech are all impacting the financial services industry,” according to Insider Intelligence.

The market researcher notes that big tech companies such as Apple and Amazon could capture up to 40% of the $1.35 trillion in U.S. financial services revenues from banks.

There’s also the all-important trust issue. A Bain & Company survey of 151,894 consumers finds 54% trust at least one tech company more than their bank.

Fintechs pay fast

Among the numerous reasons for spending more on fintech, two stand out: faster and easier financial transactions. During the pandemic, businesses needed to get paid faster than normal to cover their expenses.

It’s possible more middle market spending has shifted to fintechs – and away from banks – to take advantage of technology’s efficiency benefits, especially invoice and payment automation.

This all contributes to a surging fintech market. According to The Business Research Company, the global fintech market totaled $127.66 billion in 2018. It’s predicted to grow at 25% to $309.98 billion by the end of 2022.

Are Paycheck Protection Program (PPP) funds running dry?

The second big reason for spending declines centers on government funding. When the pandemic hit and disrupted businesses across America in 2020, the federal government passed legislation known as the Paycheck Protection Program (PPP). A CNBC report notes the program has loaned more than $780 billion to over 10.7 million borrowers.

During the two years since the program started, these businesses likely spent much of those funds to stay in business, including various types of financial services to open, close and sell their businesses along with other unusual transactions in atypical times. Overall, they needed to pay for more financial services.

But in recent months, it’s possible businesses spent less on financial services for two reasons: because their PPP loan funds have completely or nearly dried up; and because their needs for many types of emergency financial services have subsided as the economy recovers.

Rising inflation rates has shifted spending needs

The third reason for drops in spending relates to macroeconomics. During the past few months there’s been one word on the minds of businesspeople that has widespread repercussions for spending: inflation.

The annual inflation rate in the United States increased to 7.5% in January of this year – the highest since February 1982.

As prices for virtually all goods and services have risen, there’s been less to spend on financial services.

A Marcus LLP-Hofstra University Survey asked CEOs in the financial services industry how the current inflation is affecting their businesses.

Fifty-three percent said they’re being impacted by current inflationary pressures. And 28.6% aren’t affected now but will be if costs keep rising.

These statistics confirm middle market businesses now face considerable inflationary headwinds.

“Middle-market companies are challenged to manage coalescing inflationary pressures and supply chain disruptions,” said Jeffrey M. Weiner, Marcum’s chairman and chief executive officer. “Somewhat less than half of CEOs we surveyed said they are passing increased costs on to their customers, while a majority are absorbing all or some of the impact. This is forcing companies to be highly strategic in how they are managing cash flow and sourcing materials and inventory, and there is very little if any margin for error.”

What’s next for spending on financial services?

Given what we know (and what we don’t) about financial services spending, what should you anticipate going forward? Honestly, it’s hard to say.

Spending could be hindered as more companies invest in fintech solutions to provide modern solutions for both themselves and their customers.

Conversely, slowing inflation may provide businesses with more financial flexibility and encourage spending on traditional financial services.

The only thing we know for sure is that we’ll keep a close eye on this movement within our Middle Market Spending Trends Report.